Video link

Speakers

Dr. Erin B. Taylor is an anthropologist and founder of Finthropology. She specializes in how people’s financial behaviour is changing along with innovation in financial services. She holds a PhD from the University of Sydney, Australia, and has carried out ethnographic research in the Caribbean, Africa and Europe. Erin is especially interested in how culture and group belonging influence people’s actions and decisions.

Dr. Anette Broløs is a fintech analyst based in Denmark. She is an experienced network leader working with strategic innovation and partnerships, and an experienced speaker and facilitator. She holds an industrial PhD in collaborative innovation and has a background in economics. Anette has extensive work experience in finance including consultant work on the implementation of PSD2 and six years as CEO of Copenhagen FinTech Innovation and Research.

Summary

Digital transformation is rapidly changing financial services. Innovation is key, but though Financial Service Providers consider themselves innovative they are generally not perceived as such. One reason is that innovation is not just about introducing new technologies but very much about developing solutions that work in the human context. This is what Finthropology helps companies understand. We talk about what qualitative research has to offer and give examples from our own research in Brazil and Switzerland.

Erin Taylor: Anthropologist specialising in financial behaviors, focus on the micro of the human behaviors, and Annette's background is a little more in the Macro, although she does, of course, have a long history of understanding people as well, and has been very happy to join with the in this endeavor to try to bring a human perspective into understandings of finance. Focus on:

How ordinary people in different countries use financial products and how they're adapting to changes in the financial products that are available, and changes in the economy in general

Projects that look at what is happening inside financial service companies in terms of issues like gender equality collaboration between different kinds of institutions like credit unions. Example projects: a) project with Western City University in Australia, which is a five year project looking at how farmers in Laos and Cambodia are using digital financial products. b) Filing Research Institute, I I just briefly mentioned, which is examining how credit unions in the United States Very small and medium-sized credit unions are trying to um sort of stay alive in the market, and even try to thrive by collaborating with each other in different forms.

Surprisingly few qualitative research organisations that specialise in finance. Finthropology is as far as we know, the only one. Whilst data and quantitative research are great at telling you what people are doing, they are not great at telling you why people are doing it. Qual is excellent for digging down and understanding motivations, what people are actually doing on the ground, how they are making decisions and how they are engaging with each other.

Brazil study we did last year, which was collaboration with Sicpa. So we went to Brazil to look at how people were using payments, tools, in order to assist Sicpa in thinking about the future of potential CBDCs in Brazil. There is currently no CBDC in Brazil, so we could not focus on that. So what should we do? We looked at the range of payments options that people are using, including the classic thing like cash and cards, but also newer payments platforms, especially the payment platform picks, which was launched a couple of years ago Brazilian Central bank to create a platform for payments that is offered through commercial banks. So it works okay as a bit of a proxy to think about CBDCs.

First began to try to understand the context through desk research and to choose field sites to do this research. Brazil is a very large country. choosing sites can never be representative, at least are indicative of what might be happening around the country. So we chose one urban science, and also a rural site for comparison, especially because in rural areas there's often a lack of access to infrastructure one.

- Large # research questions in interviews, and also a sub-set of interviews using Portable Kit method, which is um a tide of interview where you first ask people your normal generic interview questions, and then you ask them to take everything out of their bags and pockets and wallets, cards, their phone, this sort of thing, and you ask them to explain to you, what are the financial items they're carrying, and why? And this gives you a lot of depth of information about how people live their everyday lives, which people often find it difficult to talk about, because people are not very used to talking about money.

- Observation exercises: stand in the street and watch how people were paying, whether they were comfortable, standing in the middle of the street, using their phone, whether they would take their wallet out at the last minute to pay, or whether they were quite happy to sort of stand there with money in their hand, especially to get a a sense of people's safety in different kinds of public places around the city and in the countryside.

Four insights:

Friends & Family - Mind money for them. They will lend money to each other, and so on, and so forth. This is not particularly surprising. Uh it's not necessarily the case in all countries to put in around the world. People don't always trust their friends and family. So, while not surprising, it is important to confirm one hundred and fifty

very high awareness of the risk of theft and fraud. In Brazil there are really quite a substantial number of cases involving fraud and scams, including, you know, physical theft of cash, but also cloning of credit cards, hijacking of mobile phone numbers. HIGH AFFECT how people will use cash and financial tools in different spaces, especially around the city.

mixed response in terms of whether people trusted traditional banks and digital services providers, although we did find a reasonable level of trust in banks overall. We found that where people may or may not have trusted Banking institutions, LOW AFFECT on the choices they made. So they were not a lot of examples of people saying, Well, I don't Trust Bank. So therefore i'm not going to use the bank it tends to be, people would say, Well, maybe I do or do not trust these kinds of providers. But what choice do I have? I'm going to use them anyway.

Government. So there was a general distrust of governments, but people would say. Well, you know the Government has my data, but I don't have any control. I don't have any choices to whether to hand that data over or not, so people did have concerns, but they felt they were quite powerless to have their own choices. LOW AFFECT

Main Takeaway we learned from the question of trust and investigating it we need to be more specific when we talk about who trusts who a lot of surveys out there when they sort of try to measure trust, especially in government, will sort of just ask, Well, do you trust the Government? Yes or no, or how much? But what we find is that people in Brazil and in other countries as well may differentiate more or less in terms of who in the government they trust. So in Brazil, the fear of government tended to be fairly general. People did not really seem to be able to point to specific reasons why they didn't really trust the government whereas they had very specific reasons for why they might not trust somebody who may rob them on a street late of night, or they may not trust using their credit cards in certain situations, trust tended to be more important in guiding their decisions, because it was so specific.

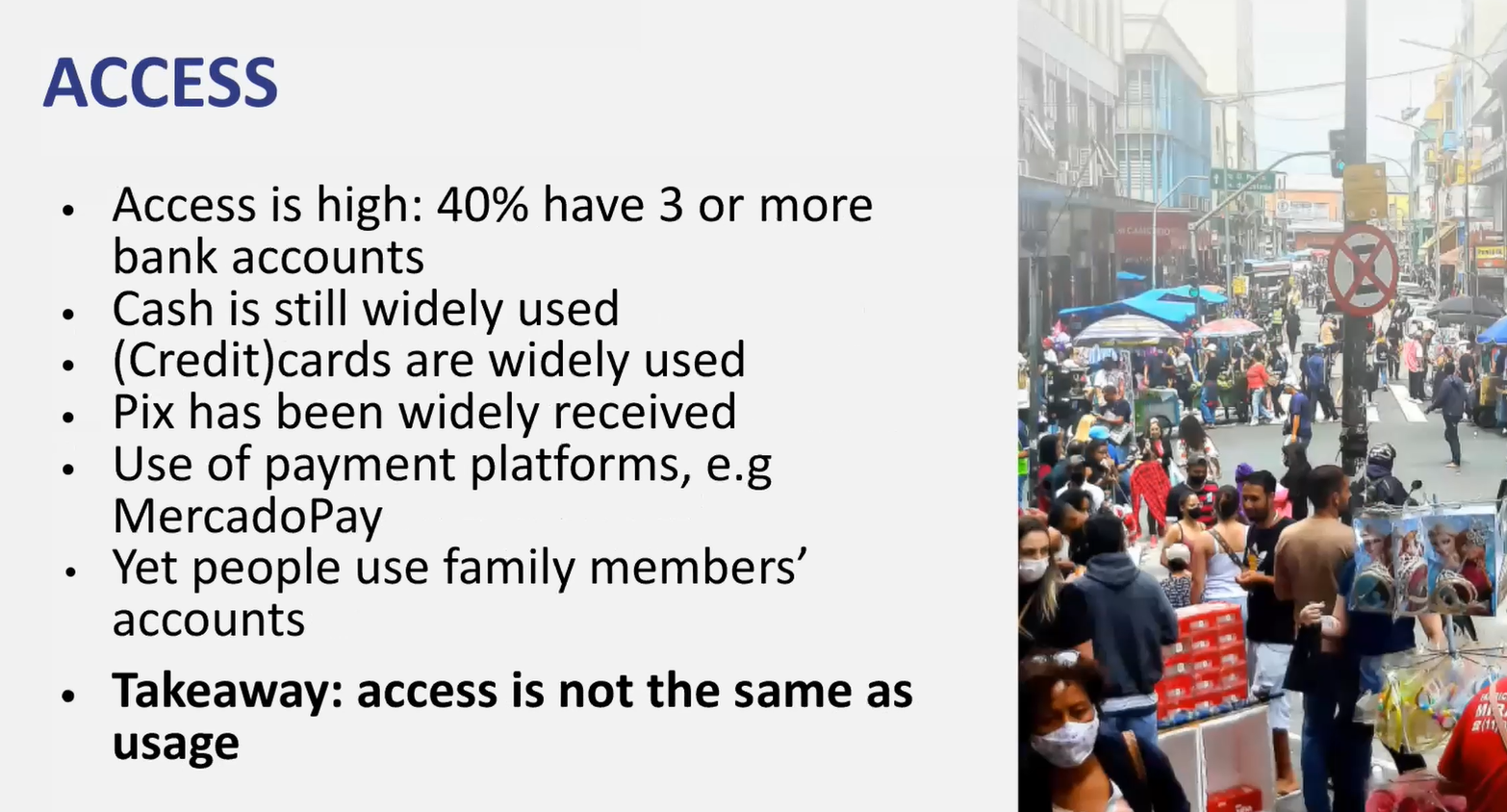

Lots of research on countries that are lower or middle income, tends to highlight an issue of access of financial inclusion. Brazil is a middle income country with quite a well developed financial system, and doesn't have many issues of access. We found that access is very high: 40% or more have bank accounts, and it's more than you would expect from the kind of financial inclusion rhetoric that assumes often that people who are low income. You may get them to open a bank account, but you may not be able to get them to engage with a large range of financial tools. We actually found the opposite

in Brazil cash is still widely used as a credit and debit cards, and the platform I mentioned earlier at Pix has been very widely received, it's being very broadly used by consumers and merchants across the country as our other platforms, such as MercardoPay

- Interesting that, despite the fact that most individuals have a high level of access on their own. There is still a great deal of account sharing between family members and friends. So you'll encounter people who, for one reason or other might have their own bank account, but they decide to use the family members. Pix identification key in order to accept payments when they're working as a vendor, or you'll find family members that share a bank accounts, not just spouses, but also children, siblings, etc, to the extent that they actually forget who the account belongs to. And so the reason why this matters is because historically, when we've talked about access to financial services.

- Access does not equate to usage. You may have a situation in a country. Let's say this has been the case in India, India has on paper a fairly high rate of financial inclusion. But a certain subset of those people who are said to have access may own a bank account or a mobile money account, but not use it so you'll have people have access, but they don't use, so the numbers can be skewed to show a degree of access. Even If people lack their own individual accounts, they may still be using financial services. So the take away here was that again, we need to be much more specific, and be much clearer on how we actually measure that access and that usage

Choice which to me was one of the most interesting findings to come out of the study. We spent quite some time trying to figure out how people choose between different kinds of payment products, different kinds of banks, and so on. And it was very interesting to try to disentangle how people made these choices. So we found that when people were choosing between banks it was relatively straightforward to figure out the logic there. So what people often do is, they have different accounts that they use in tangent in order to lower the fees they pay overall; and the reason why this is possible is because in Brazil traditional banks charge quite substantial fees for transferring money from one count to another. But they don't charge for withdrawing cash from atms, whereas the new online banks are the opposite. They don't charge transfer fees at all, but they do charge money for withdrawing cash from atm. So what you get is people being very savvy and having both kinds of accounts, and if they want to withdraw cash, they transfer money from their digital account to their normal bank account and withdraw it, and vice versa. So that was relatively easy to to certain how people make choices there.

It got to be more complicated When we tried to figure out how to people choose to pay between cash card and the Pix payment system, you may expect to see some patterns. But what we found is that people make highly individualized choices depending on questions like, is it safe? Is cash available is the ability to pay with Pix available? Difficult to pin down some sort of common thread in how people make these decisions. So, for example, some people are averse to carrying cash around because they're concerned about getting robbed, and so they prefer to pay with cards and carry no cash at all. Other people carry cash because they don't want to use cards because they're concerned that their cards will get cloned and and some people are concerned about whether Pix is reliable, and said, I prefer to use the other two. Apart from a general fear of security that did have an influence, we found very little pattern, so we think it's important to not generalize over population, and and be aware that people will make choices for a wide variety of quite personal reasons. Although it's difficult for us to discern a clear pattern, the people themselves are very clear about why they're making their choices. So we're not saying that people don't know what they're doing.

Takeaway we got from our examination of choice is that looking at people's behavior, and especially the way in which they makes choices indicate that it is possible that they see the options available to them as being kind of on par so, where they use cash or card or Pix, it's there are pros and cons to each and what this indicates to us is, there are probably gaps in people's, financial toolkits. No one tool does everything that people need, so there are probably spaces left over to be filled. And indeed, we find that if people do have access to new products and services, they will find a way to use them. If those products and services feel one of those gaps in it toolkit. So if anybody is interested in developing financial services for for Brazil, we say that it's not necessarily a bad environment,

note on financial literacy, because this is often discussed with respect to lower income populations and lower income countries, it's generally assumed that lower income people are not very financially literate. In Brazil what we found, which you may already guess is that people are very price aware. They will very much know the different prices of the bank transactions, so they can avoid fees. They will know exactly the cost of basic goods and services, and they are very good at managing their money in on to meet their needs. They will combine services to get those lower costs, and a highly capable what we think is that what we really need to do is to ensure that we distinguish between academic literacy and functional literacy. I'm sure everyone's familiar with the kind of national literacy tests that sometimes governments try to make populations take. In fact, most people, in our study were highly competent at that functional literacy,. We didn't give them any kind. academic test, so we don't know how they would score, but certainly to us it was very clear that their functional literacy was very high, and that is very important to take into account when looking at the development of new products and services. It's simply not a good idea to assume that people are somehow financially illiterate or technologically illiterate, or anything else. It's good to anticipate that some sectors of the population probably do have a low literacy in some areas, and we need to consider that in our design. But it's not a good starting point. Given that so many people are so capable

Anette Brolos:

Different background. I have worked in finance professionally for many years, mostly on strategy and innovation, and I did a late industrial Phd on collaborative innovation. So one, this is very common area for me to work with, and one of the things that I realized working in finance is that financial companies are not very good at listening to their customers. It's not at all like retailers or many other industries. Uh. So So this is really an area where there is a gap, and I think that central part is likely to fill that gap, and if i'd been really pleased to work with them for the last few years on some of these projects, and i'm going to tell you about three consecutive products that we did on female finance. We realized at some point that there were a lot happening in this area. Lots of companies set up targeting females and other incumbent players in the financial markets actually offered services directed, particularly at women as well.

- I'll just take you through some of the findings that we did, looking first at the projects that the the kind of products that these companies offer. We also looked at the type of company and how they are working

- Finally, i'll go a little deeper into the study that we did in Switzerland, where we interviewed women about their experience with me.

- General findings about financial services for women. So what it is that women like that's different from what we see in the market?

First of all, women like functional solutions, and they like things to be called what they are, and they, like, you know, finished services, support the issues that they feel in in their everyday life, so as to bring the school through the the kids through school, set up a company or manage your finances.

They like convenience, and and to be in control of the spending, and therefore we found that many women, contrary to what might have been thought, are actually quite keen on using mobile and digital solutions, because it helps them manage on the go.

Set great store for sustainable values. So is the company is the financial service provider that i'm going to talk to do? Are they aware of climate risk? Are they aware of serving the local community? Do they take gender aspects into a considerations on their daily businesses. So these are important values for women as well,

Interesting perspective is that many of the women we have talked to and listen to like to learn about, or work with their finances together, so they might want to share how to save. They might want to learn about investments together, and actually make decisions on investments together. And learning is another key aspect. We saw that many of these product providers actually offered academies or books, or other types of lessons.

Key takeaway from from this general run through all the findings is that these findings might themselves be the financial services for the future, and not just the financial services for women. Possibly what we see is that when you actually start to ask customers what's important to them, they will tell you different things then the main revenue or the main profit you can get from from investing something or the main cost that it has, or the risks involved, so that it's a totally different language, and this might be interesting for all people in the future.

Study in Switzerland. We had a Swiss partner on the study. So that was the reason why we particularly chose Switzerland. We were not able to go to Switzerland. As this was during the pandemic, so we did electronic interviews with people. We did also here a Portable Kits study. So we asked these women to bring their bags to the zoom meeting and to take out all the things that they had in them, and photograph them and share their photos with us. We also asked them to share their wallets, and their phones to see what kind of apps that we're using, and what kind of solutions they were using, and this discussions we had with them about how they learned to manage some money, who they asked for advice on money etc, would generally confirm the findings that we had from looking at the products. (Convenience, Control, Value)

We also find that although the women had very different backgrounds, they all had some kind of appetite for new solutions, a little like Aaron was telling about Brazil that they were were very aware about the possibility, so they would use wise or Revolut for their international transactions to transferring money to their kids abroad, or whatever, because it was cheaper and easier. They were likely to to take new solutions to use.

Very aware about risk, and where they would conduct transactions, and i'll come back to that a little later. That was a little wary of some types of solutions. So they would stop them slowly, slowly, and only to some point like the new mobile service which is whiskers called twin. It allows you to do P2P transfers in Switzerland. Some of the women had used it. Some were not sure that it was really safe, and some have trouble using it because they hadn't taken the full package, but only the the one where you need to top up your wallet all the time, and so that which would give them difficulties at the the retail center.

The control of money would lead to different choices like we saw in Brazil about how to use your money. So these women would use cash. In some instances they would use their credit card at the end of the months where they were. They might be worried if there were money enough in the account, and some of them would use like Revolut or Wise for for cheap international transfers.

Almost all these women told us that they felt they ought to know a lot more about finances. They ought to understand better in order to invest for their pensions. They could not buy shares because they did not understand completely the stock market, and they also were felt that they ought to do a lot more about their management of money.

Key takeaway here that when you decide it's so important to understand what actually triggers the customers need, what is it that they worry about, and what is that they need?

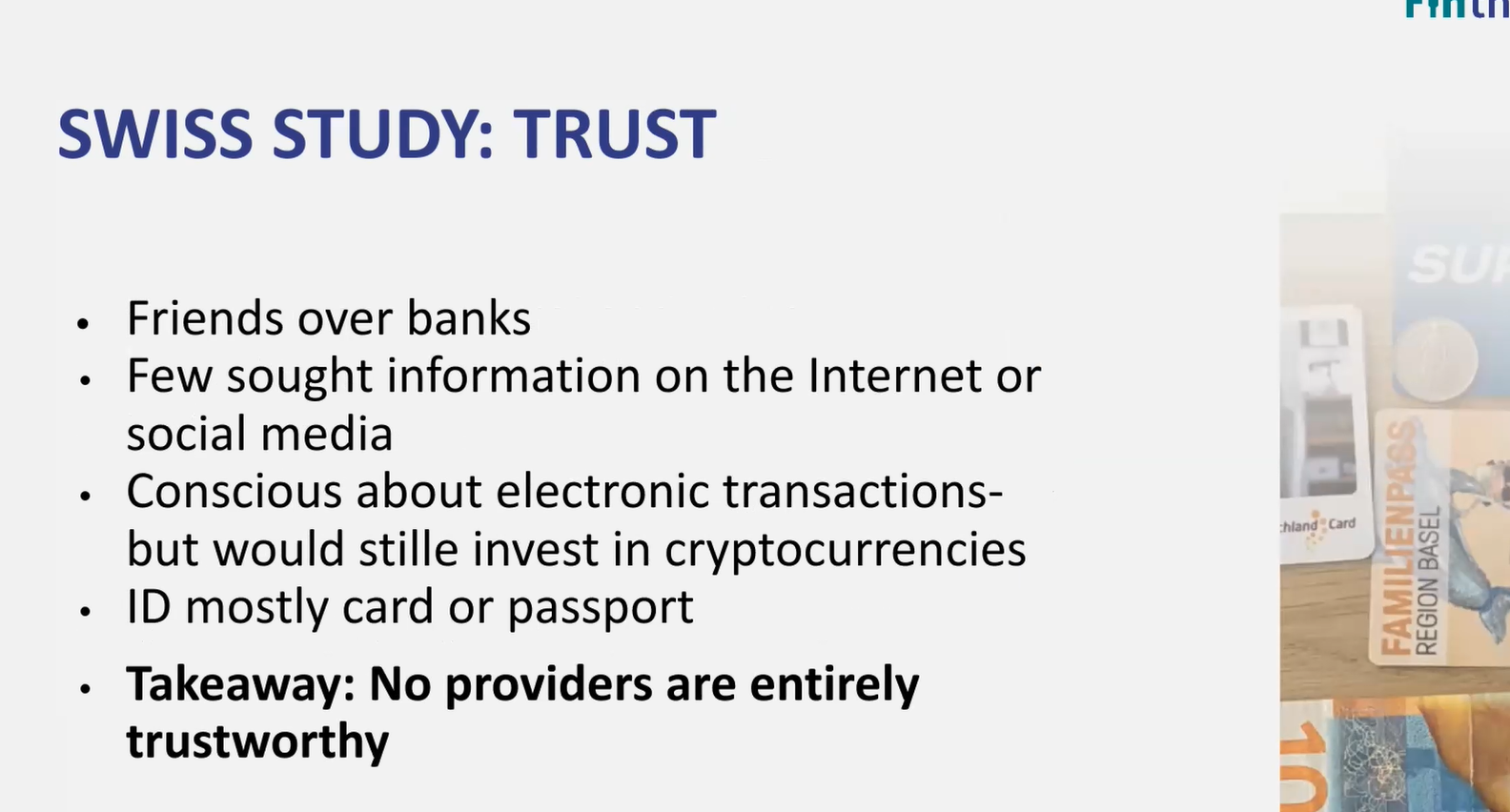

Trust issues that we find, we found we would have expected in a country like Switzerland, that people would be able to to discuss quite a lot with their bank and that they would look to all kinds of different sources for information about banking and finance in general. But just like in Brazil we found that friends and family are more important than banks. They would rather talk to their brothers or their friends, who might have some banking experience or not. Then they would talk to their bank advice. They did not feel well received. When they actually approached the bank, they would generally express that they feel condescended to, the banker would treat them as children, and not really take them seriously, which is a very bad way of meeting your customer.

Few sought information on the Internet or in social media if they followed influencers or looked for information in areas such as these. So it was really like the face to face the friends and family with the most important way of getting information in this area. Even among some of the younger women. So it it's not just a gender issue. But of course there are big variations here.

Many of these women were very conscious about how they conducted the electronic transactions. Some would say, Well, I only do my only pay my bills when i'm at home, where I use my computer, my own computer. I'll never do it in the office. I'll never use my mobile phone on public transportation to pay a bill or to make a transaction. So i'm. I'm really conscious of the risk that I run people can perhaps steal my password or see what I'm actually doing on my mobile phone. So that was quite interesting, and to find as an issue, even if they were willing to try out new services, and even if many of them said that they would actually invest in cryptocurrencies. The answer to that was actually more, a question of not really understanding the crypto currencies. So instead of the stock market, where you really need to understand, and you need to know when you should be able to know a lot of things. People felt less. These women felt less obligated to understand crypto currences, and so it was a kind of a lottery ticket. You can invest one thousand euros in cryptocurrencies, and if you lose them, that's okay, so that was one way of overcoming a trust barrier in a different issue.

- Did not talk very much about identification and other solutions, because a few of these women were into the technical space, and that was not the main subject either of our report. But we did notice that most carried plastic cards or passports as their identification. So that's an interesting aspect as well.

- Key Takeaway: Even in a country like Switzerland, no providers are seen as completely and entirely trustworthy. There are pros and cons of every provider, whether it's a Fintech or a global player, whether it's a national bank, or or even a government service. S

- Insight for when we are looking to build the the solutions for the future. So many of us grew up learning to trust authorities and institutions. So you trust your police officer, the doctor and the banker because they were the police officer, the doctor, and the banker. But of course we all know that young people turn to social media, and they look for quite different ways of trusting organizations, and people, so they will look for the values as they are expressed in different media, and they will look for social media rankings when they, when they want to decide on whether to to work with one company or another. So I think The interesting thing here is that trust is changing - It's not the same concept today as it was before, and probably tomorrow, with the changes that we see in digital solutions, it will be different again.

One takeaway to to add to this one is that we are today building the solution for the future with the knowledge of today. So I think this is what I wanted to say about our female finance studies.

Conclusion: It's so important to understand the users to understand the people. When you want to create a new solution, whether it's the CBDC or any other kind of financial product, because otherwise they're not likely to be used.

Trust is changing, and it's not uniform. You may trust the government, but not the bank. You may trust the Fintech provider, but not your local banker. You may trust the the central bank, but not your tax office

- That also means that we can introduce the perfect solution in the markets, but they need to work with the customers. That's the first thing. They also need to work in the environment that we're providing they need to work with the trustworthy intermediaries. So if the integrated areas of the solution, like a CBDC are not trustworthy, then we're not likely to see them being adopted and used broadly, which is probably why we see some differences like between the very quick and broad adoption of the Pix in Brazil, and the very slow and difficult uptake of in Nigeria,

- It's also a broader context of culture, and culture is a difficult thing to pin down, so i'll not make an attempt. But I will share an anecdote with you: In Denmark, in the 1800's, we had absolutist royal rulers who were worried about the administrators, they put in place to collect taxes and and other gains. So they into started introducing regulations and standard for good and honest behavior and State administration, and some of the some of the standards and some of the regulations that they introduced are still with us today, which is probably what you see when you look at the very high confidence and trust that the Nordic people in particular the banks have in their governments and institutions, although they get some to some extent, they are difficult to see. which goes to show the culture is a very slow process as well.

DISCUSSION

Neil Thomson What I find interesting is awareness of digital identity and how identity flows between various transactions and platforms is not terrible, but Apple seems to me grabbing great mind share in terms of their pitching about security and privacy, which is really what in the last year and a half that they've been pushing it, that it? In other words, they're buying the benefits, not the technology. Is that a reasonable statement?

Anette Broløs: Well we haven't looked so closely into all the different players in the market, and and not particularly into identity as such. We just noticed that this is a very important area, so it's difficult to follow all the areas in detail.

Pasi Sinervo: Could that be a possible solution for the future, at least into the countries. Perhaps many want to recent a bank office concretely, but that is a quite impossible, because there are not so many offices that you can with it. So could that be one solution for the future? And then it's not only the banks, it is also other financial services. We don't have any more so many desks, but many want to visit somewhere, so could that be one solution for the future. And in this first presentation what do the customers think if that is? And of course, when there is only a couple of banks, so you may be from the Mudricks, but you may trust the banks that they are real banks. But if there are several things, or do some things, then you have to question which is the most trustful partner as a bank. If there is offices, that's not so far easy. How do you find them? This was something I am interested in, when you don't have offices, how they want to use chat bots at the moment, but some like chatbots, like a virtual assistant. Some don't like. So one solution could be that you have office

Anette Brolos: I think that is a great question. So let us know if you like to do a study into this! Probably probably we will find that different people have different perspectives on whether it's better to meet on a sort of face to face, and whether other methods work for them.

Andrew Slack : I think for me as well that it it brings out a question of what value the interaction medium has. You know, potentially an online call with someone that you, you know you can. You can see them! What's the value of being kind of dislocated? Is it that an individual, who perhaps can't get to a physical location? And that's the value of having that kind of a conversational interaction? And then, in that case, what additional value on top of that, with something like a virtual environment can bring? I think these are the open questions for me.

Erin Taylor

Can I just add something to that. It's not exactly an answer. It's more of an extension. We're actually working on another project, which is about CBDC and is in in four different countries around the world, and there's been some interesting findings that in some countries where people heavily rely on bank agents who go out into the field. They start seeing the individual who visits them as being the bank so they'll have the same agent visit them, you know, week after week, and for them the bank fades into the background. They actually come. Sometimes they can't even remember the name of their bank, but they remember the name of the person who represents that bank. So we're looking at kind of polar opposites in terms of how people are engaging face to face or online online around the world,

Richard Zbinden : We found that basically somehow we have to replace the physical, and especially if I go into the Meta words, or if I do, communication, that is or not, where i'm not able to test. If i'm really talking to this person to the right person identity becomes a very trusted, trustworthy identity, will become a very big issue, because today if I meet somebody on Linkedin, then I have no clue of his profile is independent of a big providers,

Anette Broløs: I like your comment about underestimating people, because I think you're absolutely right, and I think that was the point Erin was trying to make with the literacy perspective as well.

Nicky Hickman : So I think we go into design processes very often with the whole unconscious bias thing. Who's present in the design room, and the tech team and and the Legal and Compliance team and all the rest of it. And I really like your distinction between functional literacy and academic literacy, because this perception that all you need is education, and then all will be well with the world if they could just understand what they might, they're supposed to do with their money, for example. Whereas, actually what we need is accountability from those organizations to build trust, but also This functional literacy we need to learn from them and provide services to support those those functions. So fascinating work, and lots to explore in that.

Erin Taylor: Certainly lots to do with respect to literacy. I have felt for a long time. Now that the biggest literature literacy issue with respect to financial services is simply understanding the ever-increasing array of products and providers that are out there. That's a real challenge, Actually, that's a bigger challenge than than the financial leaders in the data that i'm just doing in the office themselves.

Nicky Hickman: What do you think about the really basic stuff that just being, I mean, I was really struck by your comments about access to crypto-currencies. Because, you know, I feel in many areas it's a sense rather than being built on solid research. Regular financial services, even like credit cards, are opaque in their presentation, and that's where you get miss-selling and part of the risk around for example, loan sharks. If just basic things, like savings, accounts and loans and mortgages and borrowing were simplified in their presentation about the rights and responsibilities, What kind of a difference that would make?

Erin Taylor: Do we need more or less financial literacy these days? Because, on the one hand, we have all these apps and things that will help us make decisions about even things like investment. But, on the other hand, information is absolutely so opaque. So we had a great discussion around the ways in which capacity can backfire on people as well. So there's there's a lot to discuss.

Nicky Hickman: and what do you think we could learn from the way the kind of economies and financial literacy that's displayed in, say, gaming environments with things like the Vbucks. So yeah, people often say the same thing that they say about women about youth. They don't understand finances. And yet these guys are acquiring value, trading value, making new stuff in the metaverse, if you want to call it that. All the time they they have this underlying literacy about the exchange of value, even if It's not financial, you know.

Erin Taylor: Yes, you cannot assume that people will have the same financial goals today as they did, you know, twenty, fifty years ago the changes over the generations. We need to stop assuming that just because young people don't make the decisions that you know their parents did that somehow. It means they're not financially literate, and they don't know what they're doing that we need to look more into what their motivations are rather than assume It's a literacy issue

Anette Broløs: But it's another interesting issue in this, because I think that we have some idea that it's very important to keep things very simple, because that will make it easier for people. But just like you say young people, and I think us also, people in different age groups actually manage quite complex financial issues when they want to work with them, and it's also a question of. We often have the discussion that our mortgages in the In some of the Nordic countries like in Denmark are based on the issue of bonds, and you can buy back the bonds, which is actually some kind of option who is working here, and yet everybody will over the dinner table discuss when they're going to change their mortgages. They don't feel in any way embarrassed. And I think that's because of the transparency. So maybe the actual mathematics are complex, but they understand the basics of what they're doing and that is probably key in transparency. It needs to be transparent, like you say, in plain English, but it can be complex behind, and that goes for all age groups.